The ambition to triple nuclear energy exists – now what?

Late last year we noted that support for the global pledge to triple nuclear energy by 2050 continues to grow. This month, after the Nuclear Energy Summit in Paris on March 10, 2026, South Africa, Belgium, Brazil, China, and Italy have added their names to the list, bringing the total number of signatories to 38, almost double the number that initially signed in Dubai in 2023.

But is this a reasonable and achievable target? In last year’s preview of its World Nuclear Outlook Report 2025, based on governments’ stated nuclear ambitions, the World Nuclear Association (WNA) has shown that global capacity could reach 1,428 GWe by 2050 – not only meeting but exceeding the 1,200 GWe tripling goal.

Early this year, the WNA has issued the full World Nuclear Outlook report (we recommend you read it). And it provides some very interesting insights for the future of nuclear that should help to focus industry efforts to deliver on this ambition.

Meeting the report’s targets requires unprecedented scale-up. Annual grid connections would need to increase from 14.4 GWe per year to 65.3 GWe/yr by the end of the period, roughly double the historic peak build rate seen in the 1980s.

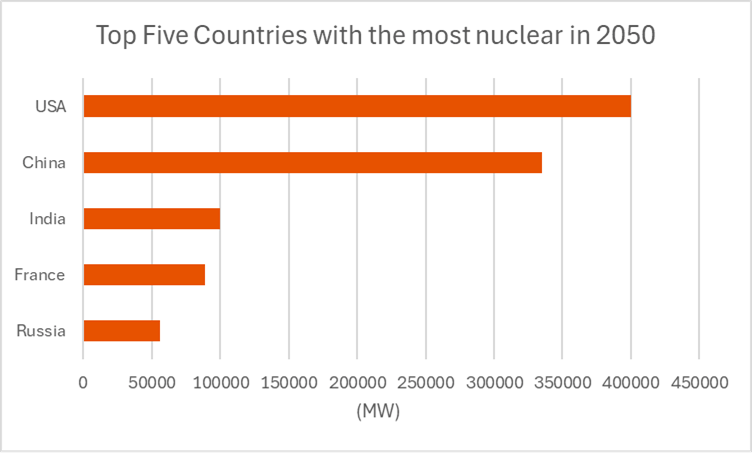

A key finding is that the growth is highly concentrated with just five countries, China, France, India, Russia, and the USA, accounting for nearly 980 GWe of the 2050 capacity, representing two-thirds of the global total. Meanwhile, countries new to nuclear demonstrate the technology’s expanding appeal, with 20 newcomer nations collectively targeting 157 GWe by 2050.

This concentration means that major reactor vendors will be overwhelmingly focused on their domestic markets. China’s vendors face building 275 GWe of new capacity at home. American vendors would need to scale up to construct 300 GWe domestically (larger than the entire current global nuclear fleet outside of the US). French, Russian, and Indian vendors face similar domestic pressures as will Korean and Canadian vendors (numbers 9 and 10 on the list).

Of the 20 newcomer countries, three, Bangladesh, Egypt, and Turkey have reactors under construction and Poland is well on its way to starting construction on its first unit. As for the rest, where will the vendors, construction expertise, and supply chain capacity come from to serve these markets when traditional suppliers are consumed by domestic demand?

The emerging small modular reactor (SMR) industry is a potential source of supply, but at this stage of their development, SMR vendors themselves face the challenge of moving from design to deployment at commercial scale.

The Declaration to Triple Nuclear Energy is a crucial political milestone, now supported by 38 countries. The World Nuclear Outlook Report confirms the goal has traction among its signatories. The world has the political will. The technology exists. The opportunity is huge. Now, the question is whether the global nuclear industry can organize itself to deliver at the required unprecedented scale.

We think that while far from guaranteed, the answer is yes, if we do the right things. What are the right things? We will provide some of our thoughts in future posts. One thing is certain. It has never been a more exciting time to work in the nuclear industry.