Nuclear Energy Summit – Broadening the nuclear coalition

In our last two posts we looked at the pledge signed by more than 20 countries at COP28 in Dubai to triple the amount of nuclear globally by 2050 and the pledge made by more than 120 companies in the nuclear industry to meet this challenge. This month we comment on the first global Nuclear Energy Summit held in Brussels March 21, 2024.

The summit photo had Brussels’ Atomium as its backdrop (Image: Klaus Iohannis/X)

This summit, organized by the IAEA together with Belgium, included senior government delegations from 32 countries, coming together for the sole purpose of discussing the future of nuclear energy and its role in supporting countries’ climate and energy security goals.

The list of 32 countries includes 14 additions to those who signed the nuclear pledge at COP28 (not all COP28 signatories participated in this event). This includes new countries with long histories of nuclear power like Argentina, India, Pakistan, and Slovakia, to those who are active nuclear newcomers (Bangladesh, Egypt, and Turkey) and those who are aspiring to bring nuclear power to their countries (Philippines, Saudi Arabia, and Serbia). The list also includes China, who has 55 operating nuclear plants and another 36 under construction, the world’s most active nuclear program, and Kazakhstan, the world’s largest supplier of uranium.

Just the fact that the summit was hosted by Belgium is important, given that it only recently abandoned its plan for a full nuclear phase out. And add Italy to the list of countries who have not been supportive of nuclear in the recent past.

The resulting declaration stated “We, the leaders of countries operating nuclear power plants, or expanding or embarking on or exploring the option of nuclear power … reaffirm our strong commitment to nuclear energy as a key component of our global strategy to reduce greenhouse gas emissions from both power and industrial sectors, ensure energy security, enhance energy resilience, and promote long-term sustainable development and clean energy transition.”

The declaration identified a range of topics where policies need to evolve (for a more complete description refer to the WNA release) including increased financing, workforce development. and support to nuclear newcomer countries. We will discuss each of these items in future posts. They are all critical to a healthy growing global nuclear sector. Why is this important? Because rather than continuously debate whether to pursue nuclear, the discussion has finally moved on to collaborating to create the necessary conditions for success.

In support of the government’s declaration, global industry associations released a joint statement noting their strong support to ensure governments can meet their nuclear ambitions. In addition, a group of 20 NGOs from around the globe issued a Declaration on the Future of Nuclear Energy jointly calling for the efficient and responsible expansion of nuclear energy.

This first nuclear summit shows the collation of countries, industry and NGOs supporting and actively promoting nuclear power is growing rapidly. It is unprecedented in the level of national leader support for nuclear since President Eisenhower’s Atoms for Peace speech 70 years ago. The time has come for action, and the stage is set to put in place the necessary policies to enable the rapid scaling of nuclear in meeting all our climate and energy security needs. The future is bright. But the work ahead is hard. This is only the beginning.

[Complete list of those signing the declaration: Argentina, Armenia, Bangladesh, Belgium, Bulgaria, Canada, China, Croatia, the Czech Republic, Egypt, Finland, France, Hungary, India, Italy, Japan, Kazakhstan, Netherlands, Pakistan, Philippines, Poland, Romania, Saudi Arabia, Serbia, Slovakia, Slovenia, South Korea, Sweden, Turkey, United Arab Emirates, UK, and the USA]

Tripling the global nuclear fleet will require massive capacity building

In our last post we looked at the pledge signed by more than 20 countries at COP28 in Dubai to triple the amount of nuclear globally by 2050. This month we consider the pledge made by more than 120 companies in the nuclear industry to meet this challenge and support a tripling of nuclear power by 2050. This is all part of the Net Zero Nuclear initiative started by the WNA (World Nuclear Association) and ENEC (Emirates Nuclear Energy Company) calling for unprecedented collaboration between government and industry leaders to at least triple global nuclear capacity to achieve carbon neutrality by 2050.

Some of the companies that have signed the industry pledge Source: WNA photo COP28 December 2023

Tripling the global nuclear capacity is no small feat. Today there are 437 reactors in operation with a combined capacity of about 400 GW. Tripling means adding another 800 GW by 2050. In a combination of large nuclear and new Small Modular Reactors (SMRs), this would mean anywhere from 800 to 2500 or so new units being built around the world. Currently, there are 61 units representing about 68 GW under construction, only 7.6% of the way there. And two thirds of these units under construction are in or exported by China and Russia. In other words, the western nuclear industry has a long way to go to do their part in achieving this lofty goal. The question is then, how can we get there from here and why is this pledge so important?

Some say it is a pipe dream. We say the first step in solving any problem is to clearly define it. In this case, to express an ambition – and that was clearly set out at COP28. Understanding the need, the question then becomes how the industry can scale to meet this demand? This requires a rapid increase in development of both the global supply chain and the human talent needed to deploy at this scale.

This is huge change for the industry. It is (except for China, Russia and possibly Korea) used to being in a global market with few new projects and too many suppliers. On top of that there have been many false starts on a renewal (or renaissance) in the past that did not work out. So, the industry has been reluctant to make the necessary investments to support the capacity building needed.

The first step is to firm up this new demand. This must be driven by government. And it has begun. Already since COP, France has announced its plans to build 14 new EPR2 units by 2050 and the UK has issued its nuclear plan on how it will meet its target of 24 GW by 2050. The UK document is clear in that capacity building and human workforce development is a critical part of this plan. Here in Canada work is underway to look at how to scale to meet 2050 growth projections as well. The US has a lot of work to do to determine how to deliver its ambition of 200 GW of new nuclear by 2050. And yes, where will the resources then come from for projects in Poland, Czechia, Estonia, Slovenia, Bulgaria, Saudi Arabia, South East Asian countries and the many possible nuclear newcomers in the global south?

The nature of global competition will also change. There will be enough work to support multiple vendors, both for traditional large nuclear and SMRs. To be successful, there must be a focus by each vendor on delivering fleets of their designs to be as efficient as possible. This can then support development of global supply chains with sufficient capacity and the human talent needed for delivery. The potential volume of work will encourage productivity improvements resulting in more on time and on budget delivery at lower total cost.

To meet the goals of net zero by 2050 and global energy security, the effort to build industry capacity is required now. All countries interested in new nuclear need to work on developing the people they will need to succeed. The ambition is clear – now is the time to act.

Nuclear project structures – it’s about managing risk

In our recent post on nuclear project financing, we noted the importance of reducing risk to investors to ensure projects can raise sufficient competitively priced capital needed to build them. Today we will discuss project structures. What are they and why are they important?

The project structure is how the project is organized contractually to build the plant and then sell the electricity to the market. Good structures help the project to succeed while poor ones end up with lawyers arguing where to lay blame rather than people delivering on their commitments.

Source: pexels.com

There are four major categories of participants in a large energy project.

The customer – who needs the energy and pays for it to be reliably delivered to their home or business;

The owner/operator (yes these can be separated, but we will keep them together for simplicity), who is responsible for building and operating a generating station to provide the energy to the customer;

The contractor(s), who have technology, design, and construction capabilities to build the plant; and

The investors, who provide the funding to support this construction and who will be repaid during plant operations when there are revenues from selling electricity.

When talking about contractual structures, the primary relationships are between the owner/operator and the customer (market structure); and between the owner/operator and the contractor (project structure).

There are a whole range of contractual structures for both relationships. Some are simple and some are complex. None are perfect. Historically, electric utilities tended to be vertically integrated monopolistic companies, often owned by governments, who were charged with delivering electricity to customers at low cost. Utilities carried most project risks and passed them on to the customers. A government regulator was charged with setting rates for customers (while looking out for their best interests) based on the utility costs and performance.

Poor project performance and a belief that competition would incent better results led to a shift to deregulated markets in many jurisdictions in the early 1990s whereby the utilities would be broken up and generators would have to compete to sell their electricity to the market. (We wrote a previous post on why these deregulated markets do not work well for building new low carbon generation.)

Being forced to take on more risk by their customers, owners wanted more certainty of outcomes and believed contractors, as the experts in performing the work, were in the best position to take on these risks. Wanting this work, contractors agreed to take on more project risk, for a price. This provided a sense of security to the owners that their risk was limited, and that they could rest easy, knowing it would be up to others to ensure successful project delivery.

Unfortunately, this has been proven to be nothing more than an illusion. In reality, the contractor’s ability to take on additional risk is limited and when project costs increase, they will generally make a claim for a change in scope requiring additional funds. This often results in contractual disputes that slow down project progress and negatively impact company relationships. In the end, there is no escaping the project risks for the owner, as it is their project and their money. After all, there is no scenario where the contractor fails, and the project succeeds.

The lesson is that when developing project structures, the objective is to manage risk while incentivising the behaviours from the project stakeholders necessary for project success; not to decide who suffers the most in the case of failure. Because for long term commercial success, there is one truth. All costs must be borne by the customer. There is no one else (unless government provides a subsidy in which case taxpayers are involved which is a different discussion – we will talk about the potential role of government in mitigating risk in a future post). When the investors state that they do not want to be exposed to excessive risk, what they mean is that they want a credit worthy borrower who can reliably replay loans and deliver a return on equity. And while ensuring they are contractually protected from risk is important, the best way forward is to confidently deliver projects to cost and schedule.

This is changing the way that projects are structured to more collaborative models whereby all parties’ objectives are aligned, and everyone sinks or swims together. Good project contracting is important in defining the project, but on its own is insufficient to ensure good project outcomes. Successful project delivery results from good project planning, doing enough work upfront to set a realistic cost and schedule; and excellent project management, supported by a high level of transparency together with a strong set of project metrics to enable informed rapid decision making to keep the cost and schedule under control. Continuously improving the ability to deliver successful projects to cost and schedule will ensure that nuclear power can meet its full potential on the road to a Net Zero future.

In 2022 the world acknowledged that net zero needs nuclear – in 2023 it will realize it needs a whole lot of it

Early last month, Vogtle Unit 3, the first new nuclear plant to be built in the United States in decades, went critical, meaning it started to nuclearfission and move down the path to producing its first electricity and becoming operational.This was great news as the project has had a troubled history of delays and cost overruns. Once fully operational the Vogtle site will have four operating units and be the largest nuclear operating site in America.

But this was not the most important nuclear news coming out of the US this past month. On March 21 the US Department of Energy released its “Pathways to Commercial Liftoff”, a set of reports to strengthen engagement between the public and private sectors to accelerate the commercialization and deployment of key clean energy technologies. This included a report on “Pathways to Commercial Liftoff: Advanced Nuclear” in which the DOE estimated a need for an additional 200 GW of advanced nuclear by 2050 on the path to net zero. This is a huge change from the past (equivalent to tripling the current fleet) when most felt that nuclear would struggle to play an important role in the country’s future.

Source: istockphoto.com

And the US is not the only country to set huge nuclear ambitions. In December of 2022 in Canada, the Ontario Independent Electricity Operator issued a report, ”Pathways to Decarbonization”, in which it suggested Ontario may need another 18 GW of new nuclear to complement its current 14 GW fleet.

In the UK, the government has set a target of 24 GW of nuclear by 2050 delivering about 25% of UK demand. In France, work is underway to deliver 6 new EPR units followed by another 8 by 2050 for a total of about 22 GW of new nuclear.

Meanwhile South Korea, after suffering an administration that wanted to phase out nuclear energy, is planning to expand its nuclear fleet in its 10th Basic Plan for Electricity Supply and Demand (2022 – 2036). The plan includes 6 new 1.4 GW units coming into service and nuclear reaching 34.6% of electricity generation by 2036 as coal use declines. And even in Japan, 12 years after the accident at Fukushima caused by the Great Tohoku earthquake and tsunami, has adopted a plan to extend the lifespan of nuclear reactors, replace the old and even build new ones as part of its commitment to fighting climate change.

This commitment to large new nuclear fleets is not only by countries that have nuclear power, but even those just planning their first plants. For example, Poland, Europe’s largest coal burning country, is planning at least 9 GW of new large nuclear plus a range of small nuclear power plants by 2040.

Why is this important? In the last year more and more governments have accepted that nuclear power must be part of any climate plan that achieves net zero targets by 2050. Nuclear was accepted (albeit marginally) in the European taxonomy as a low carbon technology, the UK is defining nuclear as green, and many other governments have noted there is no path to net zero without nuclear.

And then there is the war in Ukraine increasing concerns about energy security to a level not seen in many years. This is hastening the movement away from fossil dependence which further supports the energy security strengths of nuclear power.

So, if 2022 was the year that governments around the world finally embraced nuclear power as a necessary part of the path to net zero, 2023 will be the year they start to accept this means building a whole lot of it, expanding the global nuclear fleet at a pace and scale not seen before. What does this mean for the global nuclear industry as it readies itself for this massive increase in demand? This is a topic for another day.

So ended a year of major steps forward for the nuclear industry in Canada.

Source: pexels.com

Nuclear power produces about 15% of the Canada’s electricity with operating plants in two provinces, Ontario, and New Brunswick. In both provinces nuclear power is essential to their electricity generation with Ontario getting about 60% of its electricity from nuclear while New Brunswick uses it for about a third.

This year the federal government made its view of nuclear clear when the Canadian Minister of Natural Resources stated unequivocally there is no path to net zero without nuclear power and included funding to support this statement in its 2022 budget.

Here are some of the major achievements for nuclear in Canada in 2022.

Both Ontario Power Generation (OPG) and Bruce Power (BP) are continuing with their combined $26 Billion dollar refurbishment (life extension) programs for their Darlington and Bruce plants respectively. These programs are going extremely well, both on time and on budget. OPG has completed it first unit and is in the final stages of reassembly of its second while BP is in the final assembly phase of its first. These projects are being executed brilliantly to the point where OPG has recently been awarded second place for the Project Management Institute’s global PMO (Project Management Organization) of the year award.

OPG announced it is assessing the feasibility of refurbishing the Pickering nuclear station, currently scheduled to shut down in 2026.

Bruce Power, already the largest nuclear operating site in the world, is working to increase the output of its site by 700 MW by 2030 through unit uprating

OPG is moving forward with its first grid scale SMR project, a BWRX-300, at its Darlington site and has started site activities this year as well as submitting an application to the regulator for a licence to construct. This unit is expected to produce first power around the end of 2028. The Canada Infrastructure Bank has announced an investment of up to $970 Million for the early works of this project.

OPG is also a partner in Global First Power, who are in the process of establishing the first micro reactor, a USNC MMR, at the Chalk River site. Licensing activities are underway.

New Brunswick has announced it is working with two SMR vendors (Moltex and ARC) to establish SMRs in the province. The Belledune Port Authority (BPA) says an ARC-100 providing energy for hydrogen production and other industries could be in operation by 2030-2035.

SaskPower has selected the BWRX-300 for its first nuclear plants in the province to be in operation in the mid 2030s.

Alberta is contemplating nuclear using its ability to generate heat to help it decarbonize its oil extraction.

And there is more. But you get the point. Nuclear Power is alive and well in Canada. But why is this important? Because when it comes to nuclear as a solution for climate change, in Canada, we are walking the walk. We have a vibrant industry currently demonstrating that complex large scale nuclear projects can be completed on time and on budget. Based on this success, we have the confidence to take on First of a Kind (FOAK) risk by building the first of more than one SMR design setting the stage for global fleet deployment. This is only the beginning. With demand for clean energy increasing, we can expect to continue with life extensions (refurbishment), new SMRs and yes, even new large nuclear.

And most of all, if a jurisdiction like Ontario, Canada with an already heavily decarbonized electricity system producing well under 100 kg/kWh of carbon is saying it needs to more than double the nuclear fleet to fully decarbonize; just imagine what other jurisdictions still heavily dependent on fossil fuels need to do. The world needs nuclear power and lots of it.

Canada’s success is based on many factors, but transparency is key. Constant listening and learning assure the program continues to improve. To that end, we are ready and willing to share what has been learned to help others succeed just as we are. There is little doubt that collaboration is essential if the global industry is to meet its full potential – and we in Canada are ready to play our part.

As another year comes to an end, we want to thank you all for reading our blog and wish you a very happy and healthy 2023!

Achieving net zero requires building all low carbon technologies including lots of nuclear

In its 2022 report on the role of nuclear power in fighting climate change, “Nuclear Power and Secure Energy Transitions”, the International Energy Agency (IEA) says “Nuclear energy can help make the energy sector’s journey away from unabated fossil fuels faster and more secure.”

It goes on to clearly lay out why nuclear power is so important to a clean energy future noting that achieving net zero globally will be harder and more expensive with less nuclear.

Source: Pexels.com

The report also notes there are challenges to further nuclear deployment emphasizing the importance of continuing to reduce costs and ensure projects are built to cost and schedule. These are indeed justifiable issues and there is no doubt the industry must perform for long term success.

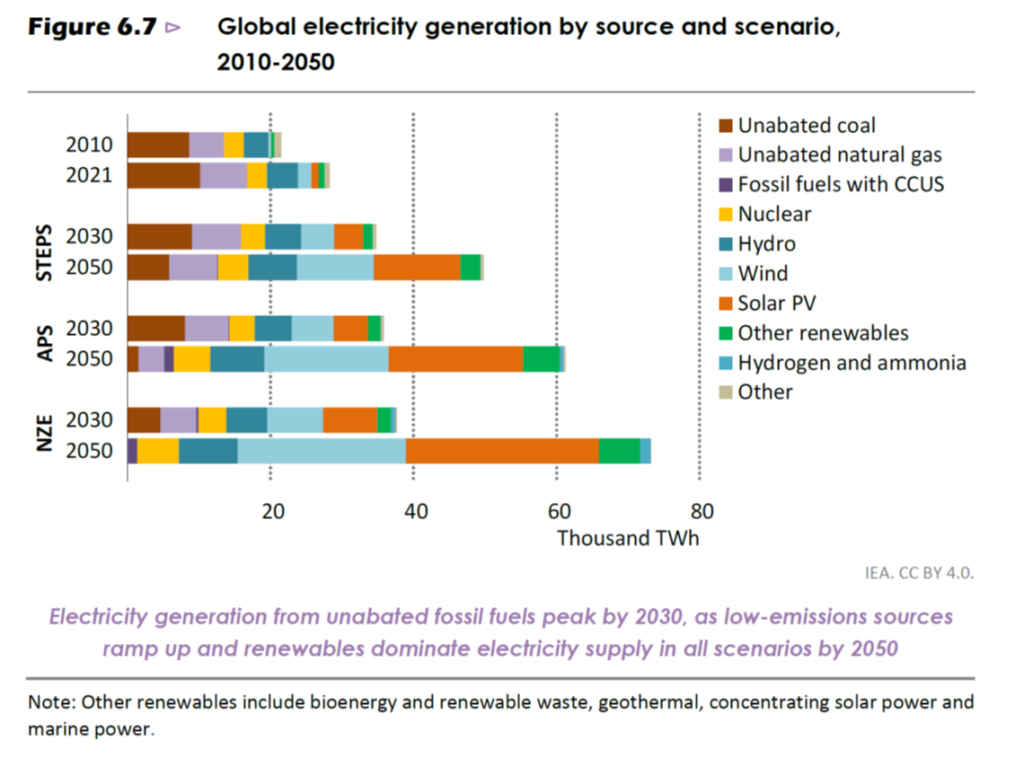

While the IEA may say nuclear is important for net zero, this has not resulted in projections for a large new nuclear program. Rather, as is shown in the 2022 World Energy Outlook (WEO 2022) just released from the IEA, the role for nuclear remains modest. Yes, there is a doubling of nuclear capacity to 2050, but because of continued electricity demand growth the nuclear share falls from 10% of global electricity supply to only 8% in its Net Zero Scenario.

On the other hand, renewables are projected to account for the majority of capacity additions over the outlook period (to 2050). In the base STEPS scenario, wind and solar PV together set new deployment records every year to 2030 and then continue with increased annual growth through to 2050. For the IEA Net Zero scenario, wind grows by a factor of 12 and solar even faster with 27 times more solar in 2050 than in 2021. The assumption when it comes to renewables growth is that there are no limits. No concern about land use, or volume of critical materials required, or how storage technology will develop to support increasing the share of renewables from its current 28% of electricity supply to 88% of a larger global electricity system. Yet we know from experience in Germany, California and others where variable renewables have successfully achieved a relatively high share of electricity supply, that system reliability suffers, often requiring fossil fuel back up to support their intermittency.

Notes: STEPS (Stated Policy Scenario), APS (Announced Policy Scenario), NZE (Net Zero Scenario) Source: IEA World Energy Outlook 2022

To be fair, we don’t blame the IEA for their views. Based on recent experience in western countries with little ongoing nuclear new build and projects that have gone over budget and schedule, it may be difficult to see a path for more rapid nuclear growth. But that certainly doesn’t mean there shouldn’t be a challenging goal. Just look at China that has built over 50 GW of nuclear capacity in the last 20 years and has approved 10 new large reactors this year alone. In the west we have examples as the US built about 100 units and France built a fleet of 59 units in less than 30 years. Twenty years ago, there was little confidence in the ability of renewables to scale and here we are today, now assuming almost unlimited growth given their success. Just as with renewables, increasing the scale and pace of nuclear new build as we have achieved in the past is also possible given the political will.

There is an international study that considers a more balanced growth for all the clean technologies. UNECE (United Nation Economic Commission for Europe) has recently released its report “Carbon Neutrality in the UNECE Region Technology Interplay under the Carbon Neutrality Concept” which takes a fresh look at how to use a broad range of technology, both existing and new to meet its net zero challenge.

This report finds “there are achievable pathways for governments to design and implement a carbon-neutral energy system through technology interplay.” In its carbon neutrality innovation scenario, UNECE considers the potential of three innovative low- and zero-carbon technologies: a new generation of nuclear power, CCUS, and hydrogen – to deliver on carbon neutrality. In this scenario nuclear grows to 3.4 times its current base in the region by 2050 (as opposed to 2x by IEA*) and reaches 27% of energy supply (compared to 8% by IEA*). It also notes challenges with all technologies. For example, it predicts 4,430 TWh of solar power in the region by 2050 (compared to the 27,000 TWh globally in the IEA net zero scenario) and notes this requires 7 million utility scale panels covering an area equal to 2.8 million football pitches equal to the entire surface area of Belgium.

There is little doubt the challenge of achieving net zero emissions in our energy systems by 2050 is enormous. Given the view to electrify everything, electricity use will at least double. To meet this growth, it has been generally accepted that nuclear power has a critical role to play, but the size of that role remains in question. Concerns about the industry’s ability to deliver has limited its potential in many studies such as the IEA WEO 2022. However, UNECE has taken a different approach and explored a more rapid expansion of all low carbon technologies, rather than assuming wind and solar can do all the heavy lifting. This seems a more viable model. Get all technologies growing as fast as possible to ensure the primary goal of carbon neutrality is achieved. We only have one world, and we need to build all low carbon technologies as quickly as we can if we really want to reach our climate goals.

* It should be noted the UNECE projects are limited to the UNECE region and the IEA projections are global.

Deregulated electricity markets don’t support a viable energy transition

In the early 1990s, deregulating electricity generation seemed like a good idea. Led by the UK, many markets rushed to dismantle their vertically integrated electric utilities with the goal of creating competition to benefit their customers, the electricity using public. The view was that utilities had become fat and lazy and since they were mostly able to pass on their costs through a regulated pricing system, they didn’t do their best to keep prices low. Competition would remove the fat.

Fast forward 30 years or so and much of the world has followed this path. There is a large relatively integrated European electricity market, the UK continues to operate its market and there are multiple states in the United States that operate this way. But is it working – and of more importance – is this the right path to support the transition to a low carbon energy system?

Source: iStockPhoto.com

To fully answer this question is a subject that requires a much longer discussion than is possible in a blog post. We will address some of the issues and explain why we believe large scale market redesign is required. For another excellent perspective we strongly recommend the book “Shorting the Grid” by Meredith Angwin that clearly explains how the current US deregulated model is failing the customer while reducing the reliability of the electric grid. Read it – please.

The original concept was sensible. Create competition in the electricity market to force electricity generation companies to become more efficient (In most cases transmission and distribution were not deregulated). It seemed to work in telecom. Why wouldn’t it work in electricity generation? And at the beginning it did work. Government owned electricity companies were sold off and broken up. New generating companies competed with existing companies and yes, the result was improved operations of the existing generation fleet.

The markets were mostly created as energy markets, where generators competed on marginal cost of production (variable operating and fuel costs) in basically real time markets to sell electricity. All that mattered was the price of electricity at any given moment. This was happening at about the same time as gas was ascending to be a major player in electricity generation both in the US and in the UK. Each generator would bid into the market at its marginal cost. The market would accept bids at the lowest cost available and continue to accept higher prices until the demand was met. The market price was the energy cost of the last generator who bid, and all participants received this price (the clearing price). When demand was high, the last bid accepted was usually gas generation which has the highest marginal cost of production and this price seemed to be enough to keep the other players with lower marginal costs but higher fixed costs content.

Then three things happened that started to change the equation.

First, at least in North America, the price of gas fell dramatically so that the only technology actually making money were gas generators. Their marginal cost had become very low given the low cost of gas and other forms of generation could no longer survive at that price. Hence the current situation where nuclear plants are closing before their end of life as they struggle to compete at very low gas prices. The US government has just launched a $6 Billion program to help save these plants. Market supporters may say – who cares? The market is the market. If gas plants are the lowest cost, then just run gas plants. And yes, that is certainly an option if a single source electricity system based on 100% gas is deemed acceptable. But if the objectives of the system are broadened to include diversity of generation for security purposes or to mitigate the risk of volatile fuel prices (yes, gas prices can and do go up), or to lower carbon emissions, then change is required.

Second, having an energy market only made it impossible to build new capacity. Since everyone was operating on marginal cost, there was no possibility to recover full costs – which is needed to support new plant investment. The solution was to create capacity markets. Payments would be made for capacity based on a bidding process so that low-cost capacity would be added to the system. Once again, in most jurisdictions, gas came to the rescue. The cost structure of a gas plant is just right for this type of market. The capital to build a plant is relatively low. Once the capacity is paid for, you only operate the plant when the energy is needed, at an energy cost that covers the marginal costs (which is primarily based on the cost of fuel).

The issue with this market structure is that gas generators were always price makers, and all other technologies were price takers. In other words, the business of electricity generation for all other technologies became a competition with gas. While these technologies made or lost money based on this competition, gas generators were always whole, no matter the price of gas. In effect, gas generation is pretty much a risk-free business in this market structure. Consumers are happy as long as gas prices are low – but will be very unhappy when prices rise.

Next, countries committed to decarbonization goals and started to support adding low carbon electricity, primarily intermittent variable solar and wind power on the system. To get these to work, subsidy was required both for price and to ensure the market takes the output of these resources when they produce, when the sun is shining and the wind blows.

To keep this story short, this structure made it near impossible for any other technology than gas or subsidized renewables to be built. Other projects were just too risky, especially those technologies like nuclear power where the bulk of the cost of energy is based on their capital investment. Even though a nuclear project is projected to be economic, once built, the price of the alternatives may change in the future so that the plant becomes unprofitable. Or in other words, no matter how successful and low cost the project, the risk of having to compete with daily changes in gas prices would be unmanageable. The solution was once again to contract outside of the market. Power purchase agreements, contracts for difference (Hinkley Point C) and other approaches were developed to support these types of projects. The result, more complexity, and complexity tends to increase costs. That is why we see the Sizewell C project in the UK moving to a Regulated Asset Base (RAB) model, to simplify the project structure and keep costs lower. (We will talk about this model in a future post.)

The reality is that data from the US DOE Energy Information Administration (EIA) show that customers do not benefit from these market structures. 2020 data shows that customers in deregulated states pay on average about 23% more for electricity than those in regulated ones. And while most states remain regulated (about 32 to 19), when you consider the actual amount of generation under both regimes, it is much closer to half of US generation is deregulated and half regulated.

Back to the point of this post. If you want to ensure grid stability, the markets need to change. If you want to encourage diversity of generation, the markets need to change. But most of all, a completely new structure has to be developed because the low carbon options (wind, solar, nuclear, hydro) have relatively high fixed costs and near zero marginal costs making an energy cost based market unworkable. For these forms of generation, a market structure based on recovering fixed costs is required.

If we really want to work towards net zero carbon emissions, now is the time to re-imagine how we are going to generate electricity and pay for it. One thing is certain. The existing deregulated model in place in many jurisdictions will not take us where we need to go and the longer we take to accept that, the longer it will be to reach our carbon goals.

Energy economics – why system costs matter

In our last post, we quoted from recent reports that clearly lay out the environmental benefits of nuclear power. This month we want to start off the year by launching a short series addressing some of the issues that impact energy economics. Today we will talk about the importance of system costs in understanding the relative costs of different generation technologies.

Last year at this time we wrote about the IEA/NEA report, Projected Cost of Electricity 2020, that shows nuclear is competitive with alternatives in most jurisdictions using the traditional Levelized Cost of Electricity (LCOE) approach. LCOE is a great way to compare costs of electricity as it is generated from two or more different options to be implemented at a single spot on the grid with similar system characteristics. With intermittent variable renewables on the system, LCOE alone no longer provides a sufficient basis for direct comparison. By their very nature, deploying these renewables add costs to the system to be able to deliver reliable electricity in the same way as more traditional dispatchable resources like nuclear, hydro and fossil generation.

Source: pexels.com

What are system costs? In a report issued by the OECD Nuclear Energy Agency (NEA), system costs (see the report for a full definition) are basically the additional costs to maintain a reliable system as a result of intermittent variable renewables only producing electricity for a limited number of hours when the resource is available (e.g. daytime for solar), their uncertainty due to the potential for days with little resource (e.g. rainy or cloudy days), and the costs to the grid to be able to access them given their more distributed nature (e.g. good source of wind but far from demand).

A 2018 study undertaken by MIT “The Future of Nuclear Energy in a Carbon Constrained World” considers the impact of nuclear power on the cost of electricity systems when deep decarbonization is desired. It looks at various jurisdictions around the world and the conclusion is always the same; the cost of electricity is lower with a larger nuclear share than trying to decarbonize with intermittent variable renewables (and storage) alone.

The reason for this impact is fundamentally due to the relatively little time these resources produce electricity. Solar and wind only generate when the sun shines and the wind blows, meaning they produce only some of the time and not always when needed. The average capacity factors of these technologies vary by location with world average capacity factor of just below 20% for solar and about 30 – 35% for wind (capacity factor is the amount of time a resource produces compared to if it would produce 100% of the time). Contrast this with the 24/7 availability of nuclear power, which can operate at capacity factors of more than 90%.

The impact on electricity systems is clear. Given the limited duration of operation of intermittent variable renewables, there is a need to dramatically overbuild to capture all the electricity needed when the resource is available to cover periods when the sun is not shining, and the wind is not blowing (all assuming there is reasonable efficient storage available which is not yet the case). The result is a system with much larger capacity than a system that includes nuclear (or any other dispatchable resource). In the MIT study for example, the system in Texas would be 148 GW including nuclear but would require 556 GW of capacity with renewables alone. In New England a system with nuclear would have a capacity of 47 GW but would require a capacity of 286 GW with renewables alone. In the UK this would mean 77 GW with nuclear compared to 478 without. And so on. The costs of adjusting the system to accommodate these much larger capacities is significant.

Since that time study after study finds the same result. This includes a study in Sweden in which 20 different scenarios for full decarbonization always come out the same; in every scenario the most cost-effective system has continued long-term operation of existing nuclear. And more recently a study in France has shown that decarbonizing without nuclear means a system more than twice as large as one with nuclear and the more nuclear in the system, the lower the overall average cost of production.

So, what does this mean for planning? The approach to implementing a reliable economic low carbon electricity grid must start with looking at the entire system. A study should assess the total costs of deploying the system under a range of scenarios using different shares of available resources. Different forms of generation have different capabilities and these need to be modelled. Once an efficient mix is determined, a plan should be put in place to implement it (i.e., X% nuclear, Y% solar, Z% wind, A% storage, etc.). When looking to deploy each technology, LCOE can be used to compare various options. For example, when comparing one solar project to another or one nuclear project to another. And of course, should the costs of any given technology vary too significantly from the assumptions in the system study that determined the efficient mix, then the system study should be updated.

Today’s energy markets are most often based on the assumption that all electricity generated is the same (to be discussed in a future post). This is true at the moment of generation when yes, an electron is an electron. Unfortunately, the ability of any given technology to actually be there to produce at the moment it is needed varies substantially. Therefore, a direct comparison of the LCOE of one option vs another is only part of the story.

To fully understand the costs of electricity generated, the costs of integrating any given technology into a reliable system must also be considered. After all, what really matters is how much we pay as customers for our electricity and the studies are clear, nuclear as part of a fully decarbonized system is always lower cost than a system based on renewables alone.

2021 – The year the nuclear energy narrative started to change

This past year, as COP26 came and went, and the climate discussion turned from emission reductions to net zero targets; more and more governments have come to accept that nuclear power should, and in fact must, play an important role in meeting their aggressive climate goals.

China is leading the way with plans to build 150 new units over the next 15 years. Other countries with plans for new nuclear include Poland, Czech Republic, Hungary, Finland, Slovenia, Romania, the UK and the Netherlands, just to name a few. In France, President Macron has stated “We are going, for the first time in decades, to relaunch the construction of nuclear reactors in our country and continue to develop renewable energies.” The US, the UK and Canada are leading the way in the development and deployment of Small Modular Reactors (SMRs). And Belarus and the UAE started up their first nuclear plants this year becoming the newest members of the nuclear family.

Source: pexels.com

We have reliable assessments this year that make the environmental benefits of nuclear power unambiguously clear from a range of multilateral global organizations.

In March 2021 the European Joint Research Centre (JRC) issued its report on whether nuclear meets the EU Taxonomy requirements and stated – “there is no science-based evidence that nuclear energy does more harm to human health or to the environment than other electricity production technologies already included in the EU Taxonomy as activities supporting climate change mitigation “.

An October 2021 study (Life Cycle Assessment of Electricity Generation Options) from the United Nations Economic Commission for Europe (UNECE) looking at a broad range of energy technologies concluded that nuclear technology has the lowest lifecycle carbon intensity of any electricity source, ranging from 5.1-6.4g CO2 per kWh. It also found nuclear has the lowest lifecycle land use, as well as the lowest lifecycle mineral and metal requirements of all the clean technologies.

Given the evidence supporting nuclear as an environmental champion, why is it such a struggle for people to think about nuclear power in a positive way? I was listening to one of the great podcasts from Dr. Chris Kiefer (Decouple podcast), (who also went above and beyond in his efforts at COP26) where he spoke to Angelique Oung earlier this year, an energy reporter and supporter of nuclear energy from Taiwan. She said it best when she said, “Before I started reporting on this issue, it (being against nuclear) is just the default position in our society. I never thought that much about it, it was just nuclear is scary, nuclear bad, nuclear old fashion, nuclear is expensive – never had reason to challenge those beliefs.”

And there is the challenge. We have discussed this before. There is a narrative of fear that goes along with nuclear energy that is part of our collective psyche. Almost every article on nuclear energy, including the supportive ones include something like “The spectre of Chernobyl and Fukushima, along with the enduring problem of nuclear waste, kept energy generated by splitting atoms on the sidelines, even if that energy was virtually carbon free.”; or ”Nuclear power can go horribly wrong and is notorious for cost overruns, but it is gaining high-profile champions.”

Nothing demonstrates this point more than when the Director General of the IAEA, Rafael Grossi, was being interviewed at COP26 and was explaining the benefits of nuclear energy. He mentioned that nobody died from radiation at the Fukushima accident in Japan – and some in the audience responded with laughter. Grossi replied “I don’t know why you’re laughing, it’s a fact. Thousands of people died because of the tsunami but there were no deaths attributable to exposure to radiation. People died also because of the evacuation, it was very traumatic,” he continued. “We’re taking this very seriously. This is not a laughable matter.”

And then something unexpected happened. Following the interview, journalist Gillian Tett decided to do her homework and learn more. As she stated, “For me, the incident acted as a (somewhat uncomfortable) reminder of the need for all of us, journalists most certainly included, to periodically question our own assumptions.” What she was found was published in an article in the Financial Times “What I got wrong about nuclear power – A debate with the head of the International Atomic Energy Agency challenged my preconceptions.” This reassessment led her to conclude “With my preconceptions about the radiation impact in Fukushima shifting, I am now doubly convinced it is time to have a wider debate about nuclear power.”

Going back to the critical comment made by Angelique, she “never had reason to challenge those beliefs.” Until now. The challenge of achieving net zero carbon emissions is massive and requires new thinking. Young people are more focused on climate issues than any generation before them. They are ready to question the entrenched beliefs of others and make up their own minds about how to solve this climate crisis. For many, being willing to take a fresh look at the nuclear option was the first step on the journey to changing their minds about this technology. As this support continues to grow, governments are becoming more willing to include nuclear in their climate plans than ever before. Who knows? 2022 may well be the year that realistic comprehensive climate plans including all low carbon technologies start to show a truly viable path to a decarbonized world.

Thank you for reading our blog. Wishing you all a very happy holidays and looking forward to more discussion in 2022.

Nuclear cost reduction: Learning lessons requires investing in people

Nuclear power is a people business. Through the hard work of many, most plants operate at very high operating factors and produce clean economic electricity 24 hours a day 7 days a week. They produce in good weather and bad, when it is sunny and when it is dark, when it is windy and when the air is still. This was not always the case. It is decades of effort by an industry dedicated to continuous improvement and learning that led to this outcome. Utilities collaborate and participate in groups such as the Institute of Nuclear Operators (INPO) and the World Association of Nuclear Operators (WANO) to ensure that operators have access to industry best practices and then they work hard to implement them at their own plants.

This process of continuous learning has not yet been fully achieved when it comes to building new plants. Here the experience is more regional with some countries like Korea and China having great success, and others struggling with new build projects that have been both behind schedule and over budget. A new report by the OECD Nuclear Energy Agency (NEA) addresses this issue head on. “Unlocking Reductions in the Construction Costs of Nuclear: A Practical Guide for Stakeholders” focuses on both the reduction of construction costs through a selected number of well-defined cost drivers and on the reduction of the cost of capital through the improved allocation of construction and market-related risks faced by new nuclear projects.

Back in 2018 we posted with our own three-part series on managing nuclear costs. As we noted then, large capital projects are difficult. They require a huge amount of planning, the logistics are often staggering and depend upon many contractors and suppliers, all who must perform completely in step for everything to come together as planned. The project manager is like the conductor of a large orchestra and as good as all the musicians may be – it only takes one misstep to ruin a beautiful piece of music. Strong leadership and good people are the key.

The NEA report focuses heavily on implementing the many lessons learned from existing projects to make the next projects better. As they state, “to reduce nuclear construction costs, eight drivers have been identified to unlock positive learning”.

We have all heard about the importance of having a strong “lessons learned” program. To be truly successful, the meaning of each of these words needs to be fully embraced.

First, we have lessons. These come from the difficulties identified in a project that should not be repeated, or new better ways to do things based on experience in the field. At the end of a project, you may hear there have been many lessons learned that have been collected ready for the next project. In reality, these are just lessons as we don’t yet have any evidence they have actually been “learned” by those who need them most, the people who are going to build the next plant.

“Learned” is defined In the dictionary as acquired by learning, acquired by experience, study. The operative word here is “acquired”. What we so often forget when we talk about lessons learned is that identifying a lesson is only the beginning. What is really important is to ensure the lesson is actually “learned” by the people who need to learn it and then successfully put into practice. We can only know this when the next project comes, the lesson has been applied and the results measured to demonstrate the lesson has indeed been learned with the project seeing the expected benefit.

Yes, new methods can be recorded based on previous projects that will avoid errors and improve project performance. But to really make improvements in project delivery requires the kind of learning that comes from experience and improving individual efficiencies. These lessons are carried by people, not databases. This means that to get the best project results, the same people must do the same tasks over and over again going from one project to the next.

Or as said in the NEA report – “the most effective way to reduce construction costs in the near term (early 2020s) is to develop a nuclear programme that takes advantage of serial construction with multi-unit projects on the same site and/or the same reactor design on several sites.” While it is true there are technical savings building on the same site, the largest savings occur because the use of the same workforce is maximized. As a task is completed on one unit, the same people can use what they have learned and immediately move on to the next unit and repeat the effort. This ensures the largest possible cost reductions.

We can use a simple example from our own lives familiar to us all. Who hasn’t had to do a project around the house and found a video on YouTube to show you how to do the task at hand? What an amazing tool! Yet even with the best step by step instructions from an expert on YouTube, we will still do the job much faster the second time. There is simply an experience factor in everything we do that cannot be easily transferred from person to another.

The path to success is through empowering people, providing them the opportunity to maximize their learning and then make use of this learning to continue to improve project performance. While it may sound counter intuitive, this will also fuel innovation as those with the most knowledge and experience continue to find ways to get even better. This means:

Standardizing is much more than just repeating a design. It is using the same people who have done the same work (engineers, project managers, suppliers and trades) on the previous project. They know exactly what to do and how to do it.

Recognizing there are limits to using all the same people for multiple projects – train, train and train some more to develop those that are new to the project. Avoid the mistake of training for competency and train for proficiency. Training must be managed by people who have actual experience. They must transfer not only their expertise but their experience as well.

When preparing for a new nuclear project, build the experience of as much of your workforce as is practical by sending them to participate in on an ongoing project before they start work on your project. The more people you have who are not touching something for the first time on your project, the better.

Of course, this can only be accomplished with an active new build program. The example of China and Korea and their success in lowering nuclear costs and building to schedule are cited regularly. Their strength is in the size of their programs. We have personally had much experience in working with Korea and we can honestly say, that having been in the industry a very long time, we actually know Koreans who have worked their full careers and have recently retired. Each one of them has worked on a real new build project every day of their 30 plus year careers. This kind of experience is invaluable and is why their projects have continued to improve. In the western world where new build has been paused, who can say the same?

Remember, when we talk about lessons learned, the operative word is “learned”. All the lessons in the world are of no value unless this knowledge is acquired by people and put into practice. This means collaborating to develop capabilities and install a system of continuous learning throughout all aspects of the industry, just as we have done to improve nuclear operations. After all, we only need to look at global nuclear plant performance to know this works.

This is an industry that attracts the best and brightest. Let’s give them the tools to acquire the knowledge they need, and more importantly, lets offer them exciting careers to develop the experience required to build the nuclear future we all aspire to. We have so many great lessons available to us; now let’s put the emphasis on learning them.