In 2017, the myth of powering the world with 100% renewables has started to crack

When thinking about 2017, it is easy to see the bankruptcy of Westinghouse and the subsequent cancellation of its Summer project in South Carolina as this year’s big issue. But as the year has drawn to a close, the continuation of its AP1000 project at Plant Vogtle in Georgia has been approved by the regulator and there is every expectation that Westinghouse will emerge from bankruptcy in 2018.

So while important, to us there is a much more important defining issue for 2017. It is the very real start of a movement that recognizes that powering the world with 100% renewables is a myth – and that chasing a myth will not get us to our global goal of meeting the world’s increasing energy needs while reducing carbon emissions and successfully combating climate change.

There were a number of defining moments in 2017 that highlight this change in attitude.

First there was the paper published in the Proceedings of the National Academy of Sciences, “Evaluation of a proposal for reliable low-cost grid power with 100% wind, water, and solar”, by 21 prominent scientists taking issue with Mark Jacobson’s earlier study claiming that 100% renewables is feasible in the USA by 2050. In a nutshell, the paper found many poor assumptions in the Marc Jacobson paper and ultimately finds that its conclusion that 100% renewables in the United States by 2050 is false. And how does Marc Jacobson respond to this criticism? Does he review his work, make changes and then show that his conclusion remains valid? No, he does what some would do when their beliefs are under attack, he sues. This is one of the most shameful episodes of the year. A scientist suing when others disagree with him is just not the way things are done. Science is about skepticism and continuous questioning. A peer reviewed paper that is critical of another one is to be applauded and responded to, to continue the discussion. Suing those who disagree is simply not one of the options.

Second, we saw Germany called out for its lack of progress on decarbonization in recent years while holding COP23 in Bonn late this year. While massively investing in new renewables, these are unable to take the place of its closing nuclear plants, thereby making coal king in Europe’s most polluting nation. This story shows how a 12-thousand-year-old forest that has been almost completely consumed by the country’s ravenous addiction to coal power.

Other countries have seen the light as well. The UK is strongly committed to new build nuclear and Sweden and France have realized that removing nuclear from the mix will do nothing to achieve their climate goals. In Korea, the public decided to continue with a new build going against its new government’s policy.

And finally, we saw something this past year, we have not seen before – the rise of the pro-nuclear environmental NGO – as those who care about the environment and climate change are starting to realize that renewables alone is a path to nowhere. This includes such organizations as Environmental Progress, Energy for Humanity and Mothers for Nuclear.

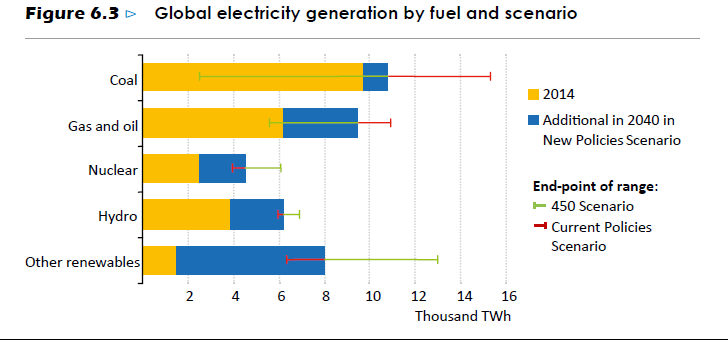

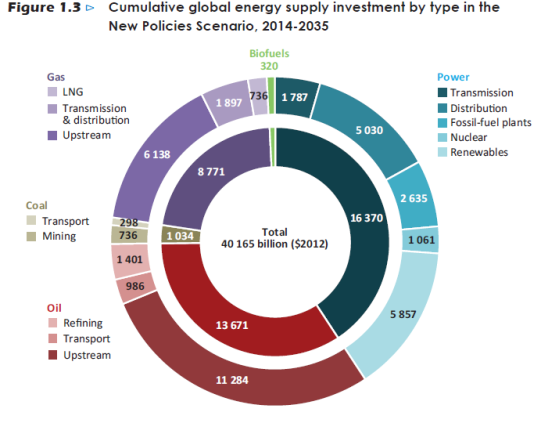

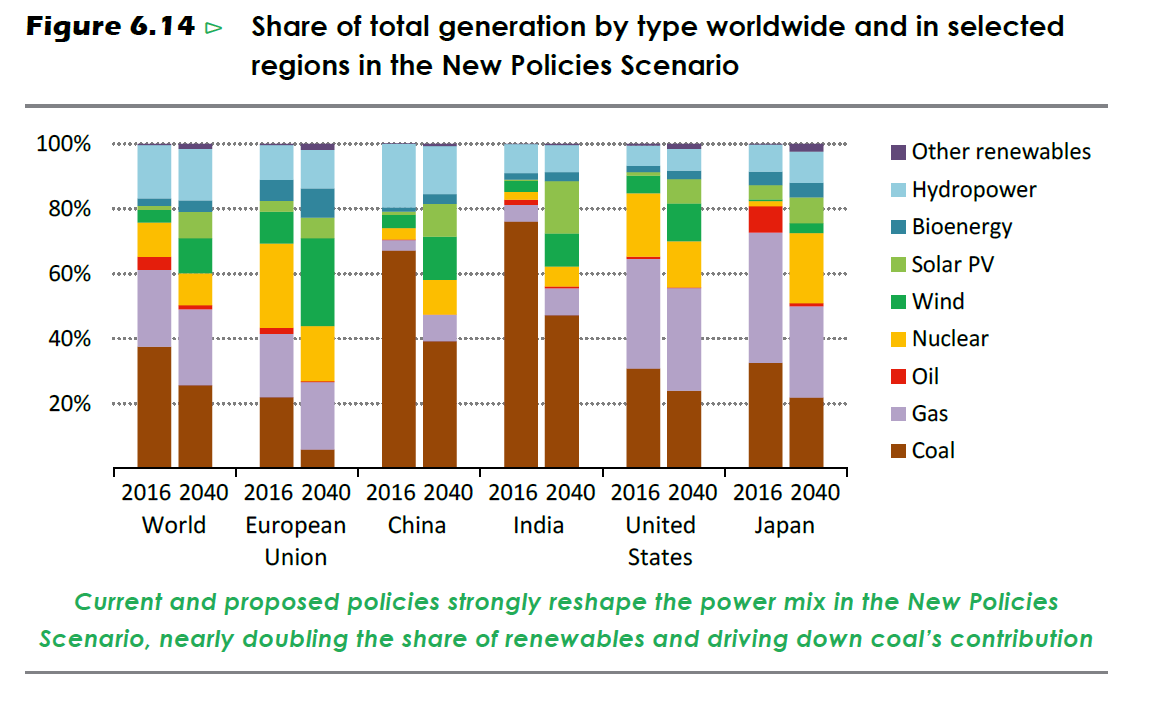

A look at the 2017 edition of the World Energy Outlook tells an interesting story.

Source: World Energy Outlook 2017

Even with massive investment in renewable technology, fossil fuels remain king in electricity generation by 2040 still producing about half of all global electricity. Wind and solar increase to anywhere from 20% in the New Policy scenario to about a third of electricity generation in the Sustainable Development Scenario (the scenario that shows what can be done to meet Paris objectives). This is even though wind and solar make up about 45% of the total investment in new capacity and global subsidy for renewables grows from about $140 billion per year to $200 billion.

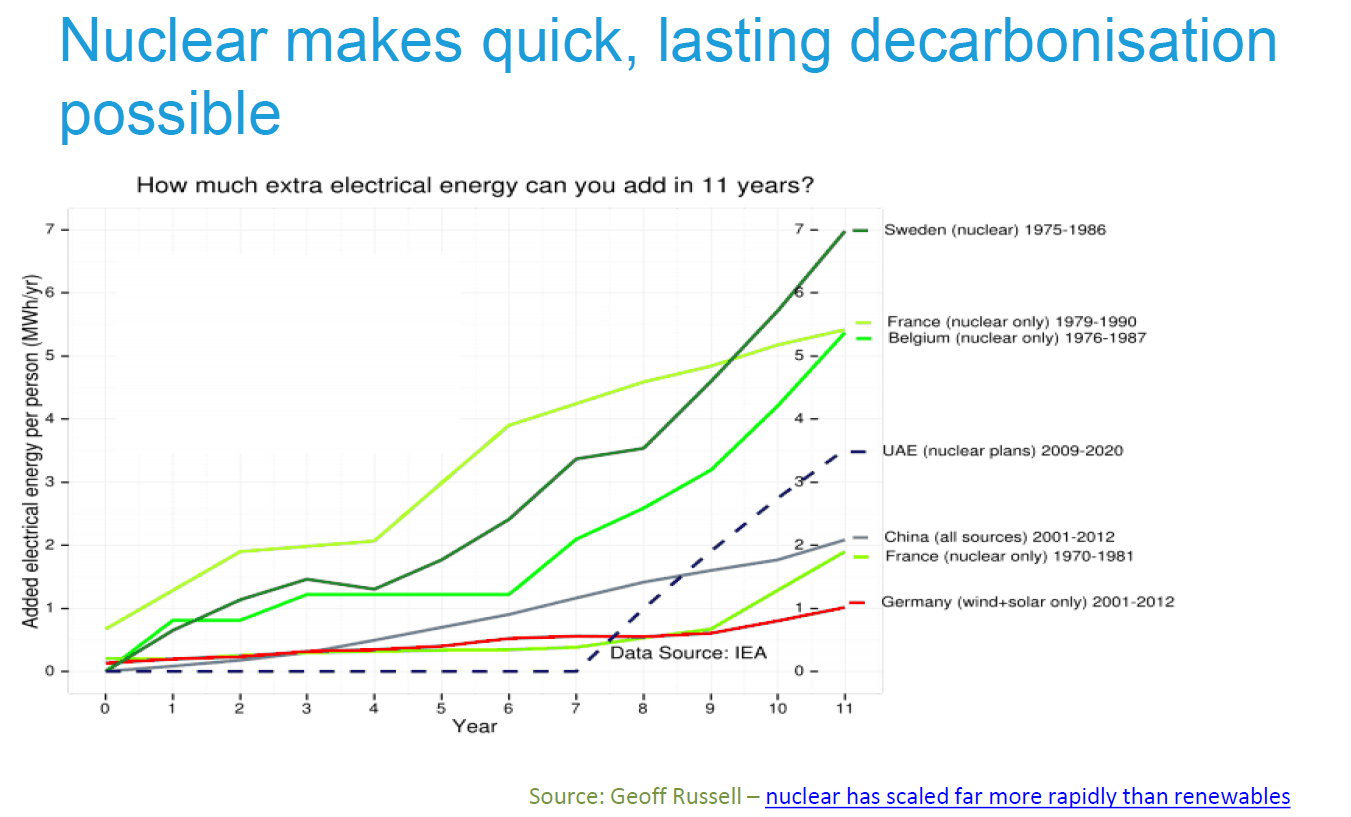

Looking deeper at the numbers, it can be seen that this investment results in a huge increase in wind and solar capacity of 5000 GW in the Sustainable Development Scenario. All other things being equal, this same amount of energy would only have required about 1500 GW of nuclear to be built since a nuclear plant produces about 3 times more energy than an equivalent size of solar plant and more than 4.5 times as much energy as wind capacity. And this is before any consideration of the intermittency of wind and solar and the needed improvements to systems to accommodate that – and of course the predominantly fossil backup needed for when the wind doesn’t blow, and the sun doesn’t shine.

What this shows is that wind and solar are good ways to reduce fossil use, probably by about 30% or so. But they are not good ways to REPLACE fossil fuels in their entirety. This must be done by more robust alternatives such as hydro and nuclear. These are the only large-scale base load options that are both reliable and low carbon available today.

And what about storage? Often, we hear that once storage technology improves, this will be what is needed for renewables to break free of their intermittency. Of course, this sounds better than it actually is. In reality, storage would be ideal for base load plants like nuclear where it can help store energy generated during times of low demand reducing the need to build new peaking generating plant. On the other hand, storing enough energy from wind and solar would require massive overbuilding of capacity to collect extra energy during the 20% of the time the sun is shining and the 30%, the wind is blowing.

Changing beliefs is hard. We live in a time when all opinions are considered valid, whether from experts or lay people. And most of all, people are challenging expert views as never before. Yes, it is a romantic view of the future to believe that all of our energy will come from energy sources such as the wind and the sun. But beliefs don’t change physics and if we really want to change the world, we need more nuclear power to replace a large portion of today’s fossil generation. Only then will we be on our way to a truly low carbon economy. We are under no illusion that this change is coming quickly, but 2017 saw the start. There are now cracks in the 100% renewable myth. It will take hard work and ongoing support from the new generation of pro-nuclear NGOs to keep broadening the crack in 2018 – and who knows? Maybe the tide will shift, and we will be on our way to a truly sustainable future.

Wishing you all a very happy and healthy new year!